Table of Contents

Galeanu Mihai/iStock via Getty Images

Cardinal Health (NYSE:CAH) has had a rough last few years staring with the opioid scandal but continues to look like a highly attractive long-term investment trading at only 10.0x forward P/E. The company fell hard last week when management reduced guidance due to further supply chain issue expectations. But this attractive 10.0x forward P/E takes that update into account and is based on management’s new midpoint of $5.33 EPS guidance. This article will look at Cardinal Health’s attractive cash flows and also give investors an estimate of the company’s current $71.72 valuation which sits around a 28% margin of safety.

Latest Results Hurt by Supply Chain Issues

In Cardinal Health’s latest fiscal Q1 2021 quarter, revenue increased 13% to $44.0 billion from the prior-year period. Non-GAAP operating earnings decreased 15% to $527 million primarily due to a decline in Medical segment profit that was driven by supply chain issues. Non-GAAP diluted EPS decreased 15% to $1.29. GAAP operating earnings were $415 million and GAAP diluted EPS were $0.94.

In the quarterly release, the company reaffirmed its fiscal year 2022 guidance range for non-GAAP diluted EPS attributable to Cardinal Health of $5.60 to $5.90. This update reflected net incremental elevated supply chain costs of approximately $100 – $125 million. As mentioned previously, this forward estimate has now been updated for an incremental $150 – $175 million ($0.40 – $0.45 EPS impact). This leaves 2022 EPS estimates at $5.20 – $5.45.

In the latest quarter, the board also approved a 3-year share repurchase plan of up to $3 billion. At Cardinal Health’s $14.7 billion valuation, that repurchase plan if fully executed would represent 20.4% of the company’s shares. As we will explore next, the company looks to have free cash flow available to support such repurchases.

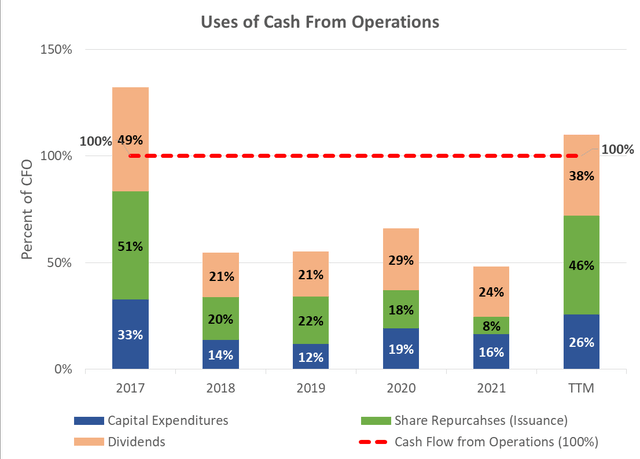

Great Cash Flow Generation

To get an idea of the sustainability of dividends and share repurchases, we can take a look at what percent of cash flow from operations is available to be returned to shareholders after making the necessary capital expenditures. As can be seen below, Cardinal Health does a tremendous job of returning cash flow to shareholders in the form of dividends and share repurchases.

Source data from Morningstar

With capital expenditures and acquisitions only taking up on average 20% of cash flow from operations over the past decade, this leaves approximately 80% to be returned to investors in the form of dividends and share repurchases. With average cash flow from operations of $2,096 million over the past five years, this 63% would imply free cash flow to shareholders of $1,677 million for around an 11.2% free cash flow yield at the current $15.0 billion market capitalization.

Notably missing from the above graph is Cardinal Health’s 2018 acquisition of Medtronic’s Patient Care, Deep Vein Thrombosis and Nutritional Insufficiency businesses for $6.1 billion in cash. This significant but one-off acquisition is not a regular part of Cardinal Health’s capital allocation strategy. It was financed with $4.5 billion of new senior notes in addition to cash on hand. This debt is already being paid down quickly in addition to the regular share repurchases as we will look at next.

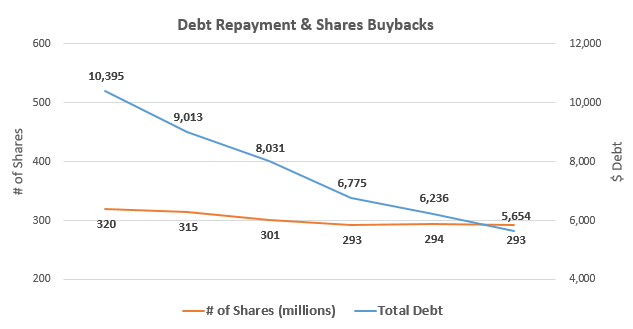

Debt Repayment & Share Repurchases

Cardinal Health has great free cash flows that are being used to deliver value to shareholders through not only the current 3.76% dividend but also significant debt repayment and share repurchases. Since 2017, the company has lowered its interest-bearing debt by 46.5% from $10.4 billion to $5.7 billion for an average repayment rate of $1.1 billion annually (13.3%). Over the same period, the company has repurchased 8.4% of their shares outstanding for an average repurchase rate of $0.5 billion (2.1%) annually.

Source data from Morningstar

Getting a Sense of Valuation

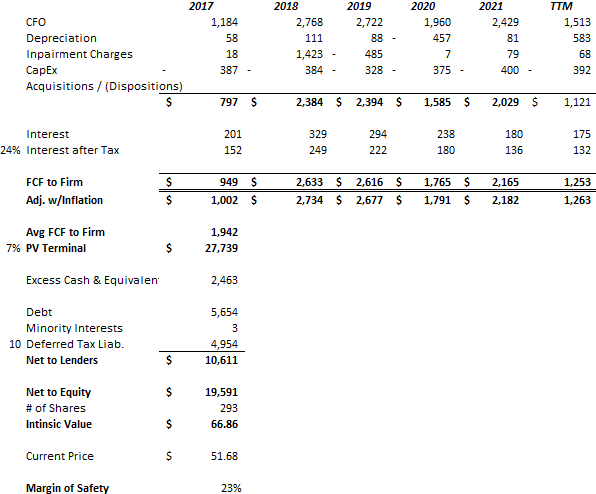

To further get an estimate of the valuation and potential returns Cardinal Health could be offering at current prices, I will use the average of the past 5 years’ free cash flow to both debt and equity investors in a discounted cash flow valuation. As can be seen in the table below, potential returns look enticing, with shares currently trading around a 23% margin of safety to the estimated $66.86 intrinsic value. Notably, this valuation subtracts off the discounted liability of $3.5 billion for the opioid settlement payout (which has previously been expensed but not paid out in cash) over an estimated 10-year remaining term.

Authors calcualtions using data from Morningstar

For those readers curious about the inputs in this zero-growth discounted cash flow valuation, here are some more details of my thought process. For a discount rate, I have conservatively used a 9% gross discount rate with a 2% growth rate given the scale, business moat, and revenue growth of Cardinal Health to arrive at a net 7% discount rate. From the present value calculation of the free cash flows to the entire firm, I have added half of the cash and equivalents from the last quarter’s balance sheet to represent the excess cash that is not needed to run the business and will probably slowly be returned to shareholders through additional share buybacks and dividends. I have then subtracted off the latest quarter’s liabilities owed to debt investors, capital leases, employee pensions, debt, and notable opioid settlements to yield the net value attributable to shareholders. This net value attributable to shareholders is then divided by the latest quarter’s number of shares outstanding to yield a per-share figure.

Risks

Cardinal Health’s scale, as witnessed by its $167 billion in revenue for the latest twelve months, and place in the health care sector makes the company significant to society but also exposed to further political pressure as seen by the recent opioid settlement. Such significant risks are unforeseen but could easily reoccur again.

Furthermore, Cardinal Health is a low-margin business with net margins between 0.19% and 1.28% (excluding the negative -2.42% net margin in the year the opioid settlement was expensed). These low margins leave the company highly leveraged operationally to pressures from COGS and operating expenses. These are the issues that are currently affecting current net income and forward estimates and will fluctuate in later years as well.

Takeaway

Cardinal Health is a nicely profitable business with great cash flows currently trading at 10.0x forward EPS estimates which already take into account significant supply chain issues. The company is a great cash flow generator and has done a good job returning this cash to shareholders through debt repayments, share repurchases averaging of 2.1% annually, and the current 3.76% dividend yield.

More Stories

How to use the Apple Health app and HealthKit

HealthIM is a very important tool for law enforcement and mental health calls

Why Australia’s newest youth mental health app shuns AI, chatbots in personalising care