Table of Contents

Willie B. Thomas/DigitalVision via Getty Images")

I spent a few years working “revenue cycle management” for a large operator of acute care hospitals, which is sort of a euphemism in that particular industry for collections, although it covers everything starting with submitting claims to insurers through collecting co-pays and deductibles from patients. During the time I spent in that line of work, it was not unusual to run into scenarios in which patients were paying multiple premiums for insurances that were incompatible with one another, specifically in the context of Medicare. To put it simply for now, Medicare participants have many offerings to select from that might give them broader coverage. However, there is generally one specific combination of products that does not work, which is having Medicare Advantage in combination with Medigap. In that scenario, regardless of whether or not the premiums are paid up at the time of claim, the Medigap coverage will not pay; it is not meant to coordinate with Medicare Advantage. Understandably, people can get confused and end up with both; the whole array of options is a challenge to navigate.

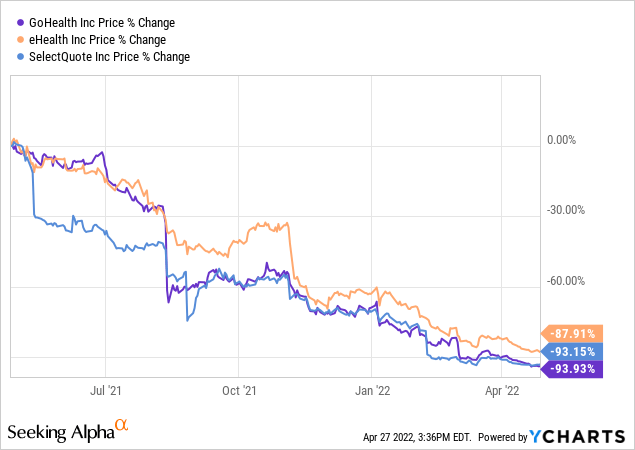

With that life experience in mind, when I noticed that online health insurance brokers eHealth (NASDAQ:EHTH), SelectQuote (SLQT) and GoHealth (GOCO) have seen serious erosion of their market value over the last year, I began to wonder what the story was. On the surface, it appeared to be a case of missing earnings estimates by wide margins.

Selling Medicare products is a major part of the revenue source of these companies, so I decided to explore if there is value in these names now. While the street has formed its own opinion, I generally like to consider the contrarian view and see what I find.

What These Businesses Are Trying To Do

eHealth and GoHealth are essentially medical insurance brokers, marketing their services as guiding those eligible for Medicare (generally those age 65 and older) to appropriate products offered by private insurers. According to the 2021 eHealth 10-K annual report, Medicare-related products account for 88% of the company’s sales. The Medicare products come in two broad categories:

1) Medicare Advantage plans, in which the consumer elects to use a private insurer, such as Humana (HUM) or UnitedHealth (UNH) for administering the Medicare benefits. These plans may come with some additional coverage options not offered by traditional Medicare, such as dental coverage, but in some other ways have some limitations, such as which providers are in-network on their plans. Medicare Advantage is full replacement for traditional Medicare plans (inpatient, outpatient, etc.).

2) The other broad category are plans known as Medicare supplement plans (referred to as “Medigap”). In this scenario, an individual has elected to use traditional Medicare benefits, but he pays an additional premium for supplemental coverage that can pay for some specific out of pocket costs not covered, ranging from the Medicare deductibles to coverage when traveling outside the United States. In order to have consistency across all sorts of variables in terms of what is and isn’t covered and makes comparisons between plans simple, these plans are standardized by a letter designation, ranging from “A” through “N” (although some plans are no longer available). Such products are offered not only by traditional health insurance companies like Aetna and United Health, but may also be purchased from a vast list of companies mostly known for underwriting life insurance, such as Bankers Life / Colonial Penn, Western & Southern Financial Group, and the list could stretch on much longer.

Why They Might Offer A True Consumer Value

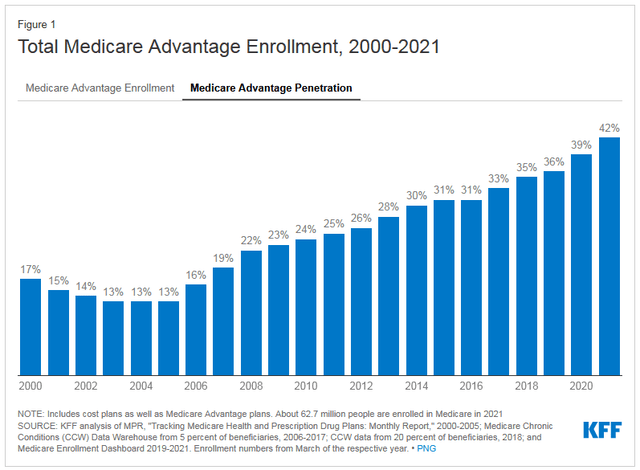

How is a consumer to navigate through these choices? Into this question enters the online brokers, each offering a path to help consumers choose. There are some definite trends that suggest such services would be positioned to do very well, such as clear overall move towards a growing share choosing Medicare Advantage. According to the Kaiser Family Foundation (or “KFF” as they are now branded), enrollment has gone from 7 million to 26 million over the last two decades, now accounting for just over 40% of total Medicare enrollment in 2021.

KFF (Kaiser Family Foundation)

If the share of Medicare Advantage share is growing, then traditional Medicare share is shrinking, limiting the pool of eligible consumers for Medigap plans. This is evidenced in part by mixed results across the full range of Medigap plans, with declining enrollments in 2020 for some categories. Overall, across all plans, there is no doubt that Medicare eligibility still has plenty of growth ahead. Through October 2021, overall Medicare enrollment stood at 63.9 million people, and is expected to hit over 80 million beneficiaries by 2030.

The Business Model and Its Challenges

The firms work as a centralized online platform where consumers can find and compare assorted policies, premiums, and make decisions for what to purchase. When a consumer buys a plan, the broker will be paid a commission, and so long as the customer keeps the plan from year to year, they will continue receive commission revenues. Being able to accurately estimate the full value on the sale of a policy has been a difficult spot for the industry as a whole. The life-time value of the insurance contract (referred to by the acronym “LTV”) has proven to be more unpredictable than originally thought, which is true across healthcare generally, but for the brokers it is also because consumers have the option of switching plans from year to year. While the forecasting of the LTV is improving, it remains a point of some reservation.

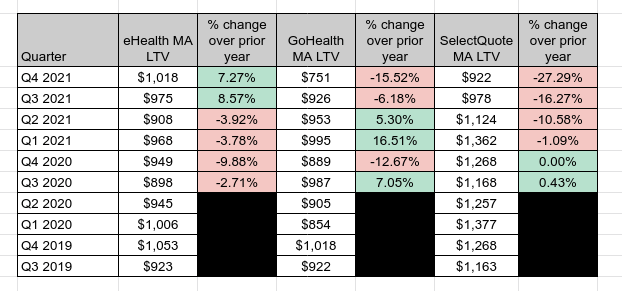

CSG Consulting, an actuarial consulting firm, has done some fantastic leg work on keeping track of the reported LTV figures reported by these three players. Since Medicare Advantage is the main driver of sales for eHealth, I will limit my comparisons to that category, but I strongly encourage interested readers to review CSG’s information on all three companies across all of their insurance categories.

eHealth, GoHealth, & SelectQuote LTV comparisons (CSG Consulting for data, author’s spreadsheet compilation)

Of the three, eHealth has kept its overall range the tightest, with no single year change in either direction of more than 10%, and has actually indicated it believes the LTVs are increasing over the two most recent quarters. Given the more negative trends of GoHealth and SelectQuote, the credibility of these LTV assumptions is quite significant. On the earnings call for Q4 2021 in early March, the eHealth CFO, Christine Janofsky, indicated:

Despite recent volatility and industry churn and the negative impact on LTVs in our sector, our member base is solid, growing and generating an increasing amount of cash per policy. The overall quality of our commissions receivable and historical reliability of our LTV assumptions is also reflected by our aggregate tail revenue.

The significantly lower figure reported by GoHealth of $750 LTV makes me a little nervous that both eHealth and SelectQuote are over-stating the values, or it could be that GoHealth will start raising its LTV estimates in the near future. Either way, the discrepancy is wide enough to take note of – I would not expect the average LTV between these companies to be so drastically different from one another.

Looking Deeper at eHealth – Costs Out of Alignment

If there is value to the consumer in cutting through the enrollment maze, then solving for how to tap into that value profitably is essential. As it turns out, it is rather costly to get customers and have enough support through the process of signing them up and keeping them. Narrowing the focus to only eHealth, who currently predicts the highest LTV for its Medicare Advantage contracts, 2021 was definitely a tough year. Revenue was $538.2 million, of which the bulk, $243.5 million, comes in the final quarter of the year during Medicare open enrollment. The accounting gross margin is pretty much meaningless, as the listed “cost of revenues” is negligible at about $2 million, but the real costs are in reaching potential customers (marketing) and enrolling actual customers (customer care). For 2021, these respectively amounted to $271 million and $179 million, for a combined $450 million, or 83.6% of revenues. Advertising is pretty self-explanatory, but the customer care is largely the cost of employing people to support the enrollment process. The net result is that those costs plus $46.3 million impairment charge to the income statement along with routine G & A and technology costs, and it is no wonder eHealth ended 2021 with a $104 million net loss.

Management isn’t blind to the cost structures being top heavy, and is looking for ways to optimize its marketing spend and reduce its customer acquisition costs. eHealth has made major management changes over the last several months, with Scott Flanders departing the CEO role as of late 2021, and Fran Soistman taking the helm, coming over from CVS Health (CVS). More recently, Roman Rariy joining the executive team earlier this spring as the chief operating officer.

Mr. Soistman outlined his top priorities for 2022 during his prepared remarks on the Q4 earning call, and while there are six he specified, they essentially boil down to: cutting costs on inefficient marketing spend and telesales staff, focus less on rapid growth and be content with slower but more profitable growth, align incentives with the insurance carriers for win-win outcomes in terms retention and commissions, and ultimately try to be less reliant on Medicare products for the company’s sales. There are some common-sense changes being implemented here, including having smaller and more localized sales teams that better understand the products available within given states (plans are carriers can vary widely from state to state) – the products and regulations can be complex, and with variations among states, expecting the sales staff to know enough about all the wrinkles is asking too much. Getting carriers on board to be willing to align their commission structure to reward customer retention is another smart move, and one it would be in the carriers own interest to consider.

Outlook for 2022

In offering guidance for 2022, management pointed to some key elements underpinning the figures. First of all, eHealth is carrying more than $900 million in commissions receivable on its balance sheet, of which $255 million is expected to be collected in 2022. Sales are being guided down by 10%, to be around $219 million in 2022, along with a $60 million cost reduction program; the net result attributable to shareholders is a predicted loss in 2022 in a range of $137 million to $114 million, certainly a bigger loss than in 2021.

I did some rough calculations based on the eHealth’s reported overall estimated membership for year end 2021, which is 1.34 million members. The current commissions receivable per member works out to be $190 ($255 million divided by the membership). Taking that same baseline and applying a 10% trim to year-end membership estimate for 2022 (based on management guidance), I wind up with current portion of receivables of $229.5 million at year-end. When combined with the rolling over portion of long-term commissions receivables, the total comes out to $888.7 million, or a reduction in commissions receivable of around $20 million, benefiting cash from operations.

Of course long-term, in a business like eHealth’s, reducing your receivables isn’t a formula for viability, as this isn’t about managing working capital management in the more traditional sense of inventory efficiency or squeezing receivables faster. Insurance contracts won’t work that way, and having a long-tail of growing expected commissions in the pipeline is better than a shrinking one. Nevertheless, it goes to show the challenge when so much of the value attributable to eHealth is locked-up in the future with the customer LTV that should slowly but steadily accrue. Getting to positive cash from operations ultimately can be aided by the working capital management, but will really sustained by starting from positive earnings, which is more than a year away at this point.

Assessing Value

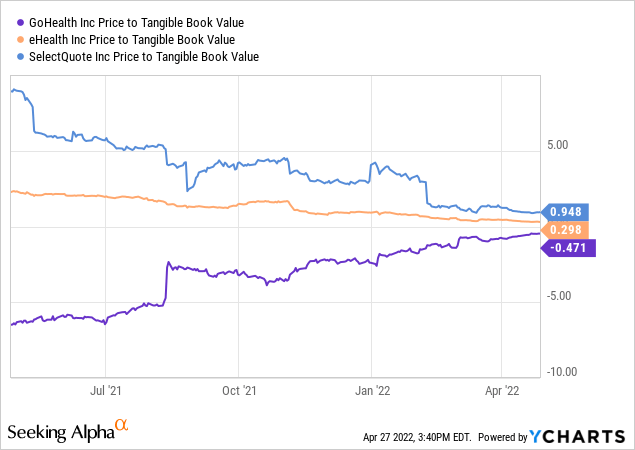

With the loss in 2021 and projected loss in 2022, determining a reasonable approach to valuation that isn’t derived from earnings will be my starting point. With such a large share of its assets tied up in the commissions receivable, I believe a price to book, or price to tangible book value is a solid metric to start with; while I might usually use this measure for sectors like banking and property insurance, a similar logic follows here, even if the multiples are much lower (in banking and insurance I tend to look for price / tangible book of less than 1 if I don’t consider the company to be distressed).

With GoHealth carrying a negative price to tangible book which suggest a distressed company (although becoming less and less negative), and SelectQuote just shy of a 1.00 ratio but having traded well over 5 times TBV within the last year, eHealth at 0.3x P/TBV has managed to sustain the most consistent valuation in spite of its drastic drop in market cap over that time. Since the overwhelming majority of the TBV is tied up in the value of the commissions receivable, I think at least two questions have to be considered in relation to the tangible book value:

- Are the commissions receivable truly high enough quality to reasonably expect them to be collected? eHealth’s answer to this is that in order to secure a $70 million loan, part of the financing was contingent on establishing the receivables’ value, and therefore involved an outside review from an actuarial firm to validate the value of the commissions figure. The result of course is that management reiterated that they are comfortable with it.

- To the extent that these commissions materialize into cash in the future, they should be on a pretty fixed schedule. For year-end 2021, about 28% of the total were current receivables, which you might not bother to discount, but the other 72% cannot be converted within 12 months. As a simplistic way to think about it, if 25% of the total is current at any given moment, the remainder would really have to be valued on some discount rate to account for the time value of the money. So unlike banks, for example, in which the loans receivable are secured by collateral making them less subject to uncertainty (and thus sporting a generally higher P/TBV ratio), the tangible book’s present value is something less than its face value.

How much less? That connects back in part to the first point – how much you might discount them is function of their relative risk. With “risk-free” rates currently rising, I don’t think a 15% discount rate is too high. For example, for simple math, using 15% on $880 million in receivables over 4 periods results in a present value of $628 million, or 70% of the full face value. For a rough sketch, I am making some quick adjustments to the TBV I calculated of $747.5 million at 12/31/21: subtract out $908 million in total commissions receivable, and add back in $628 million as a discounted present value on the receivables (assumed at $220 million per period over 4 periods discounted at 15%). That gets me to $467.5 million in TBV, and a TBV per share of about $17.50, as opposed to an original TBV per share of $26. At a current share price around $8.50 today, the price to (discounted) TBV is something closer to 0.49, instead of the 0.3x as reported.

Alternatively, to be even more conservative, I considered assigning a value of zero to all commissions receivable other than the current receivables. Reducing the TBV of $747.5 million by $653 million in long-term receivables yields an adjusted TBV of $94.5 million, $3.50 TBV per share, pushing P/TBV to 2.43x. This would be the most extreme case; there is no immediately plausible scenario in which future receivables would be (or should be) discounted to zero, but gives an outer bound. The bottom line is that I believe the P/TBV as represented at 0.3x is too low, 2.4x is too high, and determining an approximate correct value depends substantially on one’s conviction in the durability of the long-term receivables and how to treat them.

Conclusion

Intuitively, I don’t believe there is any aspect of the eHealth business that would justify it having a P/TBV over 1.0x, based on the underlying quality of the business. Obviously the market sets the price aspect, from which one can work backwards to figure an idea of the maximum TBV that is reasonable, and an investor essentially has to determine if that value makes sense.

In the range of $8.50 per share, I think the market has brought it to an appropriate range on the basis of the balance sheet’s heavy weighting to the commissions that expected more than 12 months out and the life-time value of each customer. Given the size but uncertainties of these values, even though actuaries have reviewed them, their value relative to eHealth’s ability to control its costs is where the battle lines are drawn. However, the combination of new management, an aging US demographic rapidly qualifying for Medicare, and overall enrollment trends in Medicare plans are all favorable for eHealth’s potential.

I am cautiously optimistic that the market has priced in now most of the challenges and has a more clear-eyed view of eHealth’s value, and for an investor with a long time horizon to allow the thesis to play out, I consider eHealth to be a hold or speculative buy.

More Stories

How to use the Apple Health app and HealthKit

HealthIM is a very important tool for law enforcement and mental health calls

Why Australia’s newest youth mental health app shuns AI, chatbots in personalising care